Part 2 – If Renewables Can’t Get Us There, What Will?

INTRODUCTION: What are the “Other” Options for Power Generation and Heat?

Part 1 of this Tip of the Month examined how much energy equivalence that the U.S. is currently consuming in the form of hydrocarbons, and applied an energy parity analysis to investigate how renewables compare to the energy density of hydrocarbons. Other challenges of renewable wind and solar energy were reviewed, including negative energy pricing when there is too much wind, the limitation on battery storage for base-load supply, as well as the other “hidden” costs associated with local grids that generate a significant amount of their electricity via renewable resources.

An update to Part 1, is an extreme example of the negative pricing problem that hit European markets in December of last year. According to Cornwall Insight, a period of high wind generation and low demand led to a negative day-ahead price for power in the UK for the first time on December 9, 2019. The prices for delivery from 03:00 – 04:00 local time on the hourly day-ahead auction dropped to minus £2.84 (-$3.34)/MWh [1].

At the time of negative day-ahead delivery prices, Great Britain was receiving 1.1 GW of power through two interconnectors from the Netherlands and exporting 1.4 GW through another interconnector to France. The negative value of electricity was also experienced that day in the German, Dutch and Belgian day-ahead power markets. German prices reached a low of -€16.09/MWh (-$18.90/MWh) from 02:00 – 03:00 local time [1]. For power generators/suppliers, this is a serious concern as they are financially at risk due to loss of revenue. This is a much larger scale example of the oversupply / negative value pricing issue than the examples highlighted in Part 1.

Clearly, with the limitations of wind and solar due to intermittency among others, we need other viable alternatives. This Tip will focus on the following options:

- Hydrogenation of the gas grid

- CCS (Carbon Capture and Storage)

- Gas displacing coal and oil (power generation)

- New Technology and Other Options? What do those options look like?

Part 3 of this tip will cover alternative fuels for transportation and heavy industry, and Part 4 will address the elephant in the closet, and perhaps the greatest challenge to modern society: how to attain net zero emissions.

Hydrogenation of the Gas Grid – “Blue” or “Green” Hydrogen?

The biggest question is if hydrogen is viable. “Blue” hydrogen refers to H2 that is produced via steam methane reforming using natural gas as the units feed stream. It certainly has positive attributes. When combusted, hydrogen simply produces water. The current natural gas infrastructure could be used, there are plenty of depleted reservoirs around the world available for CO2 Sequestration, and H2 has a Wobbe index that is within 10% of natural gas. Steam methane reforming (SMR) is a well understood and commonly applied technology for the manufacture of chemicals (ammonia and methanol), and for refinery operations.

The uncertainties in the viability of “Blue Hydrogen” lie in the fact that SMR has a relatively low conversion efficiency to create hydrogen (65 – 70%). These numbers do not reflect the energy requirements for the pre-combustion carbon capture, nor the energy required to compress and inject the CO2 into storage reservoirs.

Other challenges include leakage of the hydrogen (H2 is more likely to leak in current infrastructure), lower energy density (1 kWh requires 0.282 std m3 of hydrogen vs. 0.091 std m3 natural gas). One can think of this decrease in energy density as a decrease in pipeline transport capacity of hydrogen by roughly 25% as compared to natural gas. In addition, there may be a risk of possible hydrogen embrittlement for high pressure gas distribution systems. The technical and engineering issues require additional evaluation.

Two hydrogen projects are being conducted in the UK. The H21 project started in 2016, by Northern Gas Networks, the gas distributer for the North of England. Based on a blueprint of the city of Leeds, Northern Gas Networks concluded it was technically possible and economically viable to decarbonise the UK’s gas distribution networks by converting them from natural gas to 100% hydrogen, from “blue” hydrogen combined with CCS. The project has been ongoing and in 2020 with additional funding and other industry partners, they will complete background testing at the Health and Safety Laboratories, Buxton. These tests will be completed on a large variety of network assets including pipes, valves and joints and will confirm potential changes in background H2 leakage levels. They also aim to complete consequence testing in 2020 at the DNV-GL facility at RAF Spadeadam in Cumbria. This study will involve tests to confirm any changes to safety risk under background conditions, failure and operational repair on a hydrogen gas network. Once the field trials have proven that it is safe to move forward, they are planning to hold a live trial on the gas network in 2021/2022 [2].

The other project in the UK is HyNet, also located in Northern England [3]. The project is focused on enriching their natural gas network with up to 20% H2 for use in homes. They are studying SMR for H2 production coupled with Carbon Capture, Usage and Storage at Merseyside. They are also investigating hydrogen transportation opportunities. They are forecasting that the full engineering design work is to kick off in early 2020. The group estimates that the widespread use of a blend of hydrogen with natural gas could save around 6 million tonnes of CO2 emissions every year, which is the equivalent of taking 2.5 million cars off the road.

It should be noted that hydrogen generation via electrolysis of water with wind energy is possible. In some circles, this is referred to as “Green” hydrogen. This technology would fit for small hydrogen demands, but it is not cost effective nor competitive as a technology for use in generation to supply the national grids.

Carbon Capture (Usage) and Storage?

Carbon capture and storage has been practiced in a number of forms in the Oil and Gas Industry for many years. The first application of this technology is better known as CO2 Enhanced Oil Recovery, which started in 1972 in the Kelly-Snyder oil field in Texas [4]. Figure 1 provides a schematic of CO2 EOR. Historically the CO2 supply originated in naturally occurring CO2 reservoirs. Now, new projects are increasingly utilizing the CO2 captured from other industrial activities. The CO2 is injected, dissolves into the oil and carries oil to surface. The CO2 that is co-produced with the oil is separated and re-injected in a continuous loop. At the end of the CO2-EOR project, the reservoir becomes a CO2 storage site.

Figure 1. Schematic of CO2 EOR

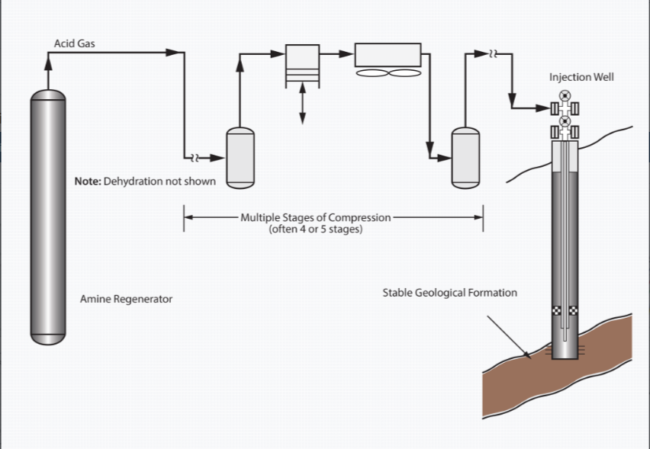

In addition, the technology of acid gas injection, as pioneered by our friends in Canada has also been in practice for many years. The first acid gas injection project was completed by Chevron near Edmonton, Canada started up in 1989 [5]. The technology started out on small volumes, but with today’s technology, very large gas rates with high downhole pressures can be achieved. The acid gas (H2S and CO2) are removed from the produced natural gas using an amine contactor, and are collected at the amine regenerator near atmospheric pressure. A schematic of Acid Gas Injection (AGI) is provided in Figure 2. For oil and gas production facilities, this technology has been well established.

Figure 2. Acid Gas Injection Schematic

The world’s first large-scale carbon storage project was developed in 1996 by Statoil off the Norwegian coast, injecting nearly 50 MMscfd into the North Sea from their Sleipner gas field production [5].

The technology for CCS on industrial facilities, however, is still a relatively “new” industry and has been slow in market uptake due to the capital and operating costs associated with it. Amine technology to remove acid gases from produced natural gas is well established. Amine technology to remove CO2 from combustion off-gas has a number of challenges due to the presence of oxygen (degrades solvent), SOx, and NOx. There are only two power plants in the world that utilize CCS.

The Boundary Dam Power Station Unit 3 is the world’s first operating coal-fired power plant to implement a full-scale post-combustion carbon capture and storage system started up in 2015 [6]. In the U.S., the Petra Nova facility, a coal-fired power plant located near Houston, Texas, the largest carbon capture and storage (CCS) in the world. The post-combustion carbon capture process started up in 2017. The CO2 that is removed from the power plants flue gas is then used for enhanced oil recovery [7].

The Netherlands is undergoing a major project to collect and capture the CO2 from three of the largest industrial ports in Europe; Rotterdam, Antwerp and Ghent. This is the first project of this type in the world and represents a major investment in CCS. The project’s plan is to construct the CO2 pipeline network in the port of Rotterdam by 2026. Once that is completed, they are planning on constructing a cross-border pipeline to Antwerp and the North Sea port by Ghent. The CO2 will be injected into two depleted gas fields in the North Sea [8]. This will be a project to keep an eye on in terms of progress and success.

The biggest challenge facing CCS is the costs associated with the carbon capture, and the compression, in particular, if the process is post-combustion due to the low operating pressures.

Gas displacing coal and oil (power generation)?

Natural gas is now becoming recognized as the best transition fuel whilst the necessary technologies and concepts for renewable or other technologies improve and mature. Secondly, gas in the form of LNG is developing a strong position in marine and transportation fuels, and this will impact on oil consumption. Natural gas in the form of CNG or LNG as a transportation fuel will be addressed in a separate Tip of the Month later in 2020.

For power generation, natural gas or LNG replacing coal can result in 50% less GHG emissions. But recognize that if one is using LNG, then 8% of the inlet gas must be combusted to liquefy LNG Natural gas provides roughly 80% of the world’s heat demands. If not planned for properly, that is not a number that will be easily or quickly replaced without severe standard of living consequences.

New Technology and Other Options: What do these look like?

Biofuels and Nuclear

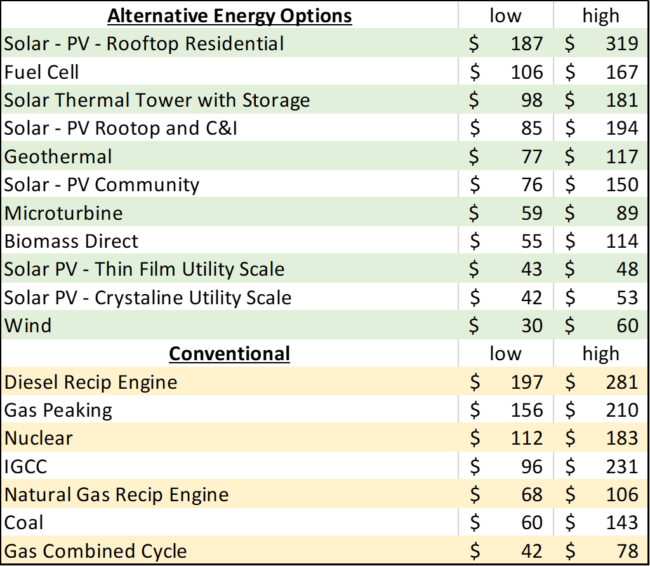

There are other options for power generation. Nuclear is an obvious choice, in that it is arguably cheaper than renewable options. It is more expensive than gas or coal, but it eliminates the concerns over CO2 emissions. The capital costs of the projects are high, and there is uncertainty around permitting and decommissioning. Germany has made the decision to opt-out of nuclear energy, France currently derives roughly 75% of its electricity from nuclear, but is planning to scale that back to 50% by 2035. The Middle East are considering nuclear options, with United Arab Emirates implementing the GCC’s (Gulf Cooperation Countries) first nuclear plant. A recent study conducted by Lazard [10], in the U.S., concluded the following range in costs levelized cost of energy (LCOE) for different energy alternatives presented in Table 1.

It should be noted that the costs in Table 1 are for generation only. It excludes the cost of integration and any costs associated for intermittent technologies. It also does not take into account reliability or intermittency-related considerations (transmission and back-up generation costs associated with wind and solar). The assumption for the Solar Thermal Tower with Storage includes a battery with only 10 hours of storage. The Solar PV (photovoltaic) Utility-Scale cost options assume a 30 MW system with no storage capacity.

Biofuels could be an option as well, but the supply of biofuels is insufficient to meet baseload energy demands. It can fit in the appropriate locality, but it is not a slam dunk alternative to natural gas.

Table 1. LCOE ($/MWh) for Alternative and Convention Power Production Options [10]

New Technology and Other Options: What do these look like?

Pyrolysis, Carbon Hub and NetPower

Scientists of Karlsruhe Institute of Technology (KIT) and the Institute for Advanced Sustainability Studies (IASS) in Potsdam have succeeded in using natural gas in a climate-neutral way. Their process is based on methane splitting, “pyrolysis”, using a liquid metal tin catalyst. Methane is continuously fed from below into a column of liquid tin kept at very high temperatures, up to 1200 °C [~2200 °F]. Pyrolysis is the thermal cracking of methane to produce hydrogen and solid carbon, effectively eliminating the need for CCS. This represents significant cost savings and makes hydrogen generation possible in locations, such as Spain, that do not have access to depleted gas reservoirs. Pyrolysis technology has been known for years, but with the older technologies, the reactors would plug with the produced carbon fines making the technology impractical for commercial applications. The new process developed by KIT does not plug and provides a carbon by-product that is valuable which can be re-used and repurposed [11]. In December of 2019, KIT announced that it is partnering with Wintershall Dea to further develop this process to an industrial scale, with the goal of having this work completed within the next three years [12].

Solid carbon or natural graphite is on the EU’s critical raw materials list and has been since the list’s creation in 2011. Europe imports nearly all of its graphite. China is the worlds’ largest supplier of graphite. Primary purposes are for steel making, but it also feeds into high-tech industries such as Li-ion battery production. In addition, graphene is becoming of great interest to many countries. Graphene s a two-dimensional atomic crystal made up of carbon atoms arranged in a hexagonal lattice. It can be thought of as a giant molecule that can be chemically modified, with potential for a wide variety of applications, ranging from electronics to composite materials. The Graphene Flagship project, worth €1bn ($1.12bn) in the EU is the largest research and development initiative to date [12].

Rice University has launched Carbon Hub, which was inaugurated by Shell with a $10 million dollar commitment. Carbon Hub will fund $100 million on research to efficiently deploy energy technologies that result in zero-emissions. The research team includes more than 70 researchers from 20 universities, national laboratories and research institutes. The research is focused on splitting hydrocarbons to produce hydrogen fuel, and solid carbon materials that can be used as building materials, components for cars, clothing, and more [14]. This research sounds very much like the work being conducted by KIT and Wintershall Dea. These two organizations will be ones to watch in the future, as this technology appears to be very competitive and can supply not only clean energy, but also a source for petrochemical feed stocks that the modern world has grown dependent upon.

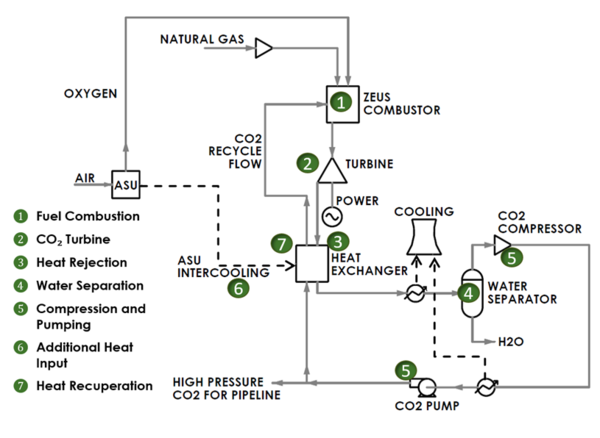

The last new technology that I would like to review is NetPower. The process uses the Allam cycle, named after the technology’s lead inventor, Rodney Allam. The process flow sheet is shown in Figure 3. Natural gas is combusted with pure oxygen, and uses super-critical CO2 as a working fluid in a semi-closed loop to drive a combustion turbine. Its byproducts are liquid water, pipeline-ready CO2, and argon and nitrogen, which could also be sold as commodities [14].

Figure 3. Net Power Schematic, Courtesy of Net Power

In 2018, the company has a started up a pilot plant near Houston, which can generate 50 MW of electricity. They have plans to scale this facility up to commercial power plant capacity of 300 MW as soon as 2021. This is another alternative technology that has significant potential in terms of the equivalent energy density of hydrocarbons and eliminating CO2 emissions [14].

SUMMARY

This tip of the month explored some of the current options being investigated to provide a clean energy solution in light of the global concerns over climate warming. It focused only on the aspects for heating and power generation. Two additional tips will be forthcoming that will review alternative solutions for transportation, and what can be done to improve our dependence on the Petrochemical industry.

To learn more about the global natural gas economy, we suggest attending our G2 (Overview of Gas Processing).

By: Kindra Snow-McGregor, P.E.

References

1. Negative Auction Prices Hit European Generators, Natural Gas News, 18 December 2019.

4. Hyne, Norman, Ph.D. Nontechnical Guide to Petroleum Geology, Exploration, and Production, Pennwell, 1995.

5. Acid Gas Injection – The Next Generation, John J. Carrol, Gas Liquids Engineering, Ltd., Calgary, Alberta Canada.

6. The Pursuit and Advancement of Carbon Capture and Storage, J. Romeo, Power, 3 March 2019

7. Petra Nova is one of two carbon capture and sequestration power plants in the world, EIA, 31 Oct 2017

8. Empty North Sea gas fields to be used to bury 10m tonnes of CO2, D. Boffey, The Guardian, 9 May 2019

9. BP Statistical Review of World Energy 2019, 68th Edition

10. Lazard’s Levelized Cost of Energy Analysis – Version 11.0, https://www.lazard.com/media/450337/lazard-levelized-cost-of-energy-version-110.pdf

11, Pyrolysis lifts prospects for hydrogen from natural gas [Brussels Conversation], Natural Gas News, 27 June 2019.

12. KIT and Wintershall Dea collaborating to develop industrial-scale methane pyrolysis for CO2-free production of hydrogen, Green Car Congress, 05 December 2019.

13. Shell and Rice University partner on hydrocarbon-based zero-emissions technologies, World Oil, 11 December 2019.